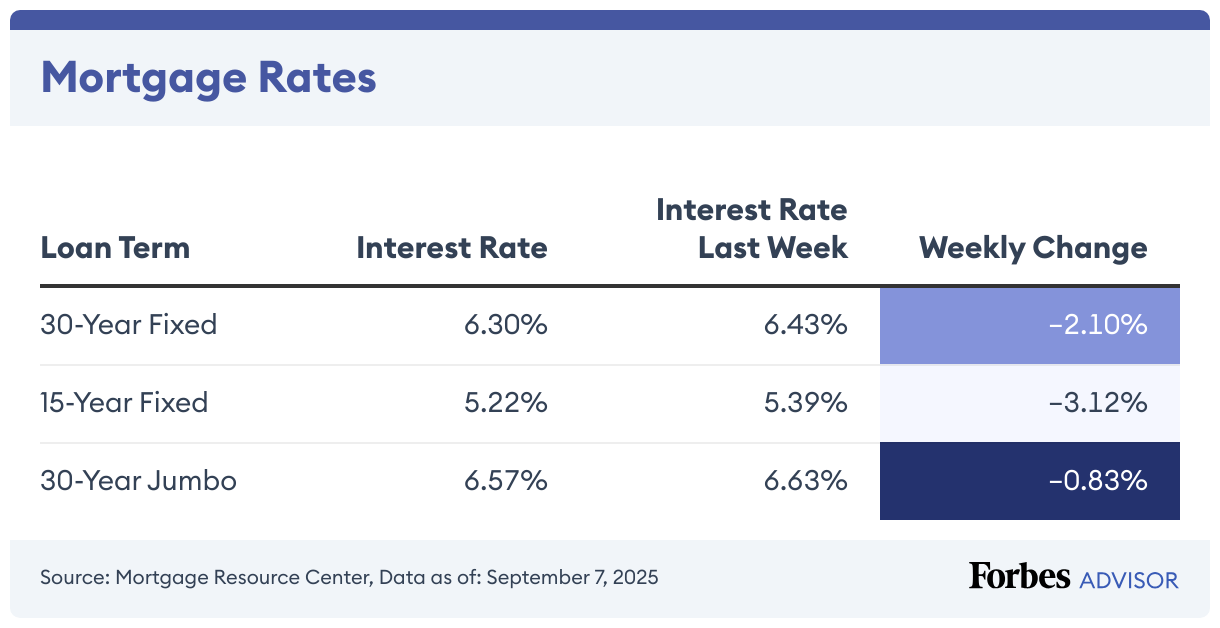

Currently, the average interest rate on a 30-year fixed mortgage is 6.22%, compared to 6.19% a week ago, according to the Mortgage Research Center.

For borrowers who want to pay off their home faster, the average rate on a 15-year fixed mortgage is 5.30%, down 0.38% from the previous week.

If you’re thinking about refinancing to lock in a lower rate, compare your existing mortgage rate with current market rates to make sure it’s worth the cost to refinance.

30-Year Mortgage Rates Climb 0.52%

Borrowers paid an average rate of 6.22% on a 30-year mortgage. This was up from the previous week’s rate of 6.19%.

Currently, the average APR on a 30-year fixed-rate mortgage is 6.25%. This is higher than last week when the APR was 6.22%. The APR contains both mortgage interest and the lender fees to help give a more complete picture of loan costs.

To get an idea of how much you’ll pay: a $100,000 mortgage with a 30-year fixed-rate loan at the current average interest rate of 6.22% will cost you about $614 including principal and interest (taxes and fees not included) each month, the Forbes Advisor mortgage calculator shows. That’s around $121,588 in total interest over the life of the loan.

15-Year Mortgage Rates Drop 0.38%

Today, the 15-year mortgage rate inched down to 5.3%, lower than it was yesterday. Last week, it was 5.32%.

On a 15-year fixed, the APR is 5.35%. Last week it was 5.37%.

With an interest rate of 5.3%, you would pay $806 per month in principal and interest for every $100,000 borrowed. Over the life of the loan, you would pay $45,618 in total interest.

Jumbo Mortgage Rates Climb 1.29%

On a 30-year jumbo mortgage (a mortgage above 2025’s conforming loan limit of $806,500 in most areas), the average interest rate rose to 6.67%, higher than it was at this time last week. The average rate was 6.59% at this time last week.

Borrowers with a 30-year fixed-rate jumbo mortgage with today’s interest rate of 6.67% will pay $643 per month in principal and interest per $100,000. That means you’d pay roughly $132,133 in total interest over the life of the loan.

Trends in Mortgage Rates for 2025

After reaching highs in 2024, the average 30-year fixed mortgage rate has remained in the mid-to-high 6% range since late January 2025. The 15-year fixed mortgage rate has hovered between the low-6% and mid-to-high-5% range.

While interest rates have fallen since mid-January 2025, experts expect them to remain relatively steady for the remainder of the year. If the Federal Reserve continues to cut the federal funds rate, it’s possible that mortgage rates will decrease in 2026.

!function(){“use strict”;window.addEventListener(“message”,function(a){if(void 0!==a.data[“datawrapper-height”]){var e=document.querySelectorAll(“iframe”);for(var t in a.data[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.source){var d=a.data[“datawrapper-height”][t]+”px”;r.style.height=d}}})}();

When Can I Expect Mortgage Rates To Drop?

Various economic factors influence mortgage rates, making it challenging to forecast when rates will drop.

The Federal Reserve’s decisions significantly impact mortgage rates. In response to inflation or an economic downturn, the Fed may lower its federal funds rate, prompting lenders to reduce mortgage rates.

Mortgage rates also track U.S. Treasury bond yields. If bond yields drop, mortgage rates typically follow suit.

Finally, global events that cause financial disruptions can affect mortgage rates. For example, the Covid-19 pandemic led to record-low interest rates when the Fed cut rates.

While a significant decrease in mortgage rates is unlikely in the near future, they may start to decline if inflation eases or the economy weakens.

How To Calculate Mortgage Payments

One of the first steps in buying a house is budgeting. To get a general idea of how much owning a home will cost, start by using a mortgage calculator to crunch the numbers.

Just input the following data to get an idea of how much a house will cost:

- Home price

- Down payment amount

- Interest rate

- Loan term

- Taxes, insurance and any HOA fees

Find the Best Mortgage Lenders of 2025

How Are Mortgage Rates Determined?

Mortgage interest rates are determined by several factors, including some that borrowers can’t control:

- Federal Reserve. The Fed rate hikes and decreases adjust the federal funds rate, which helps determine the benchmark interest rate that banks lend money at. As a result, mortgage rates tend to move in the same direction with the Fed’s rate decision.

- Bond market. Mortgages are also loosely connected to long-term bond yields as investors look for income-producing assets—specifically, the 10-year U.S. Treasury Bond. Home loan rates tend to increase as bond prices decrease, and vice versa.

- Economic health. Rates can increase during a strong economy when consumer demand is higher and unemployment levels are lower. Anticipate lower rates as the economy weakens and there is less demand for mortgages.

- Inflation. Banks and lenders may increase rates during inflationary periods to slow the rate of inflation. Additionally, inflation makes goods and services more expensive, reducing the dollar’s purchasing power.

While the above factors set the base interest rate for new mortgages, there are several areas that borrowers can focus on to get a lower rate:

- Credit score. Applicants with a credit score of 670 or above tend to have an easier time qualifying for a better interest rate. Typically, most lenders require a minimum score of 620 to qualify for a conventional mortgage.

- Debt-to-income (DTI) ratio. Lenders may issue mortgages to borrowers with a DTI of 50% or less. However, applying with a DTI below 43% is recommended.

- Loan-to-value (LTV) ratio. Conventional home loans charge private mortgage insurance when your LTV exceeds 80% of the appraisal value, meaning you need to put at least 20% down to avoid higher rates. Additionally, FHA mortgage insurance premiums expire after the first 11 years when you put at least 10% down.

- Loan term. Longer-term loans such as a 30-year or 20-year mortgage tend to charge higher rates than a 15-year loan term. However, your monthly payment can be more affordable over a longer term.

- Residence type. Interest rates for a primary residence can be lower than a second home or an investment property. This is because the lender of your primary mortgage receives compensation first in the event of foreclosure.

Frequently Asked Questions (FAQs)

How do you get a lower mortgage interest rate?

Comparing lenders and loan programs is an excellent start. Borrowers should also strive for a good or excellent credit score between 670 and 850 and a debt-to-income ratio of 43% or less.

Further, making a minimum down payment of 20% on a conventional mortgage can help you automatically waive private mortgage insurance premiums, which increases your borrowing costs. Buying discount points or lender credits can also reduce your interest rate.

How long can you lock in a mortgage rate?

Most rate locks last 30 to 60 days and your lender may not charge a fee for this initial period. However, extending the rate lock period up to 90 or 120 days is possible, depending on your lender, but additional costs may apply.

What’s the difference between a mortgage interest rate and a mortgage APR?

A mortgage interest rate reflects what a lender is charging you on top of your loan amount in return for allowing you to borrow money.

Annual percentage rate (APR), on the other hand, is a calculation that includes both a loan’s interest rate and finance charges, expressed as an annual cost over the life of the loan. In other words, it’s the total cost of credit. APR accounts for interest, fees and time.

Since APRs include both the interest rate and certain fees associated with a home loan, the APR can help you understand the total cost of a mortgage if you keep it for the entire term. The APR will usually be higher than the interest rate, but there are exceptions.

Leave a Reply